.png)

In this article, we delve into the critical shifts occurring in Web3 fundraising during Q1 2025. We will explore how investor strategies are evolving, signaling a move towards capital concentration over broad exposure.

Join us as we examine these new market dynamics, provide actionable insights for founders, and discuss the pivotal role of strategic capital in building the Web3 of tomorrow

Unpacking Web3's Q1 2025: Strategic Capital, Shifting Tides, and the Actionable Roadmap for Founders

The opening quarter of 2025 has unveiled a fascinating, albeit complex, narrative in Web3 fundraising. While headline figures suggest robust capital deployment, a deeper dive reveals a recalibration of investor strategy, one that demands founders adapt their approach to secure the right capital. At ChainGPT Labs, we're not just observing these trends; we're analyzing the underlying mechanisms to provide founders with a clear, actionable roadmap.

Capital Concentration Over Broad Exposure

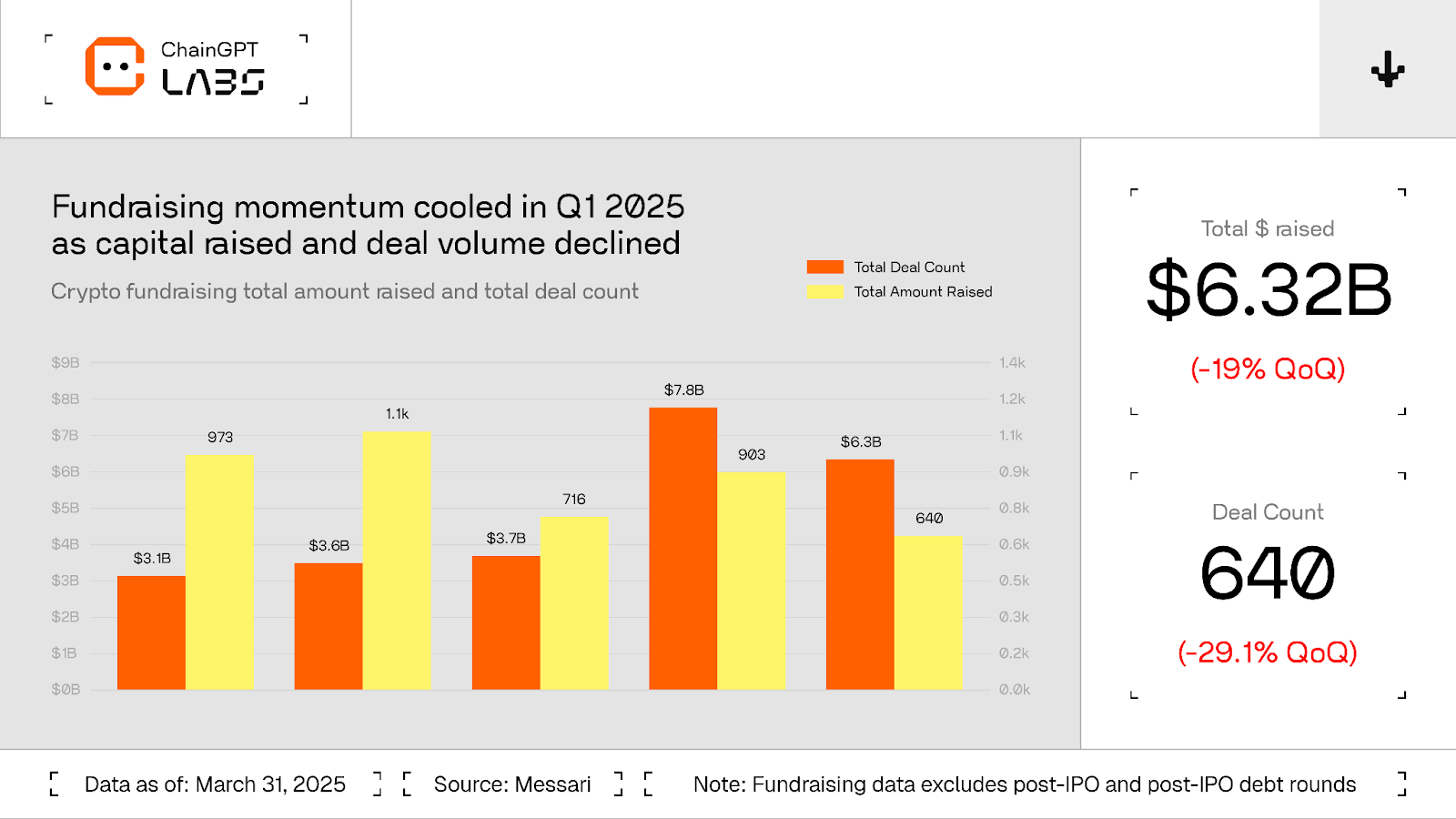

Q1 2025 saw a substantial $6.3 billion in Web3 fundraising, nearly mirroring Q4 2024's record-breaking performance of $7.8 billion. However, this impressive figure belies a critical shift: deal count plummeted by 29.1% to just 640, marking the lowest since Q3 2023. The implication is clear: investors are writing larger checks to fewer companies, prioritizing capital concentration over broad exposure.

Excluding Binance's colossal $2 billion raise (which alone accounted for over 25% of all deployed capital ), the market reflects a more "business as usual" scenario, aligning with 2024 averages at roughly $5.7 billion. This indicates resilience rather than a sudden resurgence in overall fundraising activity. This divergence underscores a continuing recalibration in investor strategy, with VCs doubling down on "category winners" and maturing infrastructure plays.

Navigating the Divided Funding Market

Our analysis at ChainGPT Labs points to several critical trends shaping the Web3 investment landscape. Founders and builders must internalize these shifts to optimize their fundraising journey:

Embrace Strategic Capital and Deep Alignment:

Strategic rounds dominated Q1 2025, drawing in $2.5 billion across just 102 deals, accounting for over 32% of all capital deployed with only 18% of total deal volume. This continues the trend of sovereign funds, crypto conglomerates, and ecosystem treasuries backing big infrastructure and Layer 1 plays. These rounds cluster around Layer 1s, middleware protocols, and token infrastructure, where alignment, not just ROI, drives capital deployment.

- Identify Synergistic Partners: Don't just chase capital; seek out investors (especially ecosystem funds and large Web3 entities) whose long-term strategic goals directly align with your project's mission. Their investment isn't just money; it's a vote of confidence, access to their network, and often direct integration opportunities.

- Articulate Value Beyond ROI: Clearly demonstrate how your project contributes to the broader ecosystem health or solves a critical piece of infrastructure for a major player. Show how your success amplifies theirs.

- Targeted Outreach: Research which strategic investors are actively deploying capital into your specific infrastructure niche (e.g., L1s, middleware, token infra) and tailor your pitch accordingly.

Master "Real Diligence" and Prove Traction for Early Stages:

Early-stage rounds fragmented. Seed round sizes fell to a two-year low ($4.4m), while pre-seed stayed strong at $2.9m. Pre-seed and seed rounds made up nearly a quarter of all deals (24%) but captured just 6% of capital deployed. This suggests valuation compression and that smaller cheque sizes are being deployed with tighter founder terms. It signals the return of "real diligence": founders need traction, not just vision, to unlock capital. The "spray-and-scale" model is clearly dead.

- Pre-Seed Resilience: If you're at the very earliest stage, capitalize on the "quiet resurgence of confidence" in pre-seed. Focus on riding high-conviction narratives like DePIN, AI-native infra, and on-chain agent tooling, as these attract accelerators, ecosystem funds, and angel syndicates. This is where capital remains most founder-friendly.

- Seed Stage Proof-Points: For seed, gone are the days of raising solely on deck and team. Investors are trimming cheque sizes and tightening terms. You

must demonstrate early metrics, user adoption, product-market fit signals, or strong distribution channels. Build first, then raise. - Data-Driven Narratives: Back up every claim with data. Even early data points can tell a powerful story of traction and potential.

Navigate the Series A Chasm with Later-Stage Maturity:

Series A continues to feel the squeeze, with only 27 rounds closed (barely 5% of total deal count). Investors appear to be skipping A rounds altogether, opting instead to either enter at seed with optionality or wait for Series B+ maturity where risks are mitigated and token strategies are clear. These Series A rounds are now priced like "mini-Bs," reserved for companies with revenue, traction, and a token strategy ready to execute. Later-stage bets are holding steady, with Series B and above seeing just nine deals but drawing in $531 million, averaging nearly $59 million per round.

- Bypass or Build: Be brutally honest about whether your project is truly "Series A ready" by current market standards (i.e., operating like a Series B company). If not, consider a prolonged seed phase to build more traction, or prepare to raise a larger pre-seed/seed to bridge the gap.

- Revenue & Traction are Non-Negotiable: For Series A, focus intensely on revenue generation, significant user growth, or demonstrable network effects. Your token mechanics should be well-defined and ready for market entry or treasury alignment.

- Growth-Stage Mindset: Recognize that later-stage rounds are less "venture bets" and more "growth-stage, quasi-private equity deals". Your pitch needs to reflect a mature business model, not just future potential.

Strategic Focus: Where Capital Flows with Conviction:

Networks took top spot in median round size ($45.1 million, skewed by Binance), with 243 investor deals, suggesting dense interest from institutional allocators. Developer Tooling attracted the most investor engagement (290 deals), but with smaller rounds ($3.1 million median), showing it remains the "long tail of infra". Consumer Infrastructure ($19.3m), Wallets ($20.7m), and Data ($24.3m) posted strong median round sizes, benefiting from a return to fundamentals: UX, composability, and data liquidity.

- Deep Dive into Infrastructure: If building core infrastructure, understand that "Networks" (L1s, scaling bets) are where capital goes to feel serious. For Developer Tooling, expect high investor interest but smaller, faster deals, often engineer-led and sometimes grant-augmented.

- Leverage Consumer Infra & Data: Projects focused on enhancing UX, composability, and data liquidity (Consumer Infrastructure, Wallets, Data) are receiving meaningful backing. These are areas where fundamental value creation is being rewarded.

- Cautious Consumer Plays: For consumer-facing projects (Metaverse & Gaming: $2.9m median, 193 deals; Entertainment: $4.65m median, 164 deals), VCs remain interested but cautious. Shift your focus from content-heavy bets to "infra-for-fun" plays – building the underlying tools and platforms that enable consumer experiences. Marketplaces ($9m median, 279 deals) and Financial Services ($11.98m median, 277 deals) also show strong engagement, particularly for transactional infrastructure and tokenized commerce.

One such example is @privy_io. Privy stands out as an infra play, they recently went on to raise an accumulated some $40M and has subsequently been acquired by Stripe for $230M.

Strategic & Private Token Sales Are Back in Fashion:

Token fundraising rebounded sharply in Q1 2025, with $1.6 billion raised across 96 public and private sales, the strongest quarter since 2022. While public sales dominated in number (69 deals, $798m), private sales ($771m across just 27 deals) rivaled them in value. This signals a pendulum swing back to concentrated, institutional token allocations. Private token deals are "bigger, deeper, and more strategic", often aligned with L1 treasuries, foundation mandates, or cross-border capital flows.

- Prioritize Strategic Private Rounds: If your project has institutional-level appeal, focus on securing strategic private token sales. These offer not just capital, but often longer-term commitment, vesting schedules, and off-market pricing that can stabilize your token's early trajectory.

- Elevate Public Sale Projects: For public sales, recognize that outside of a few blockbusters like World Liberty ($590m) , the average round was just $3 million. To stand out, your public sale needs to be a "high-trust, high-brand project" with a clear value proposition and strong community engagement.

ChainGPT Labs: Empowering the Next Generation of Web3 Innovators

The Web3 fundraising market is bifurcating; there is still cash at the idea stage and cash at the post-traction stage, but the middle is being left behind. This isn't a funding winter, but certainly a rebalancing of founder expectations. Investors are looking for sharper narratives, stronger foundations, and builders who understand how to navigate this new fundraising landscape.

At ChainGPT Labs, we provide not just funding but mentorship, resources, and a network designed to transform your vision into a category-defining project.

If you're an ambitious founder building the future of Web3, apply for our incubation program.

COMPARISON

Image

.png)

Saulius Aleksa

Paul Farhi

Tzahi Kanza

Cristian

Eitan Katz

Perry Kniest